Demand for optical connectivity remains strong despite a declining capex of telecom network operators and lower than expected growth in infrastructure spending by cloud companies. Optics takes on a larger share of the connectivity as data rates go up. Increasing complexity of high-speed optics translates to higher product pricing, boosting revenues of component suppliers, while offering cost reductions to end users in terms of dollars per Gigabit of bandwidth.

The spending of the 15 leading network operators is set to drop in 2016. The operators’ guidance on their 4Q15 earnings calls means the Far East will spend less in 2016 and in the case of the Chinese operators, significantly less. The analytics forecast that capex will be down 7% to $178 billion dollars in 2016.

The analytics estimates that its Internet Index companies will spend between $43 and $48 billion on servers, networks, and other infrastructure in 2016, up slightly from $42.6 billion in 2015. The low end of the range assumes that the spending to revenue ratio of 6.7%, seen in 4Q15, persists for all of 2016. The high end of the range assumes the 2H15 slowdown was an anomaly, and that spending grows at 15% in 2016, at the same rate that we expect revenues to grow.

Sales of optical networking equipment were stubbornly flat over the last several years and growth projections for this market are modest. Sharp declines in sales of legacy hardware, increasing use of white boxes and pluggable optics by end users dampen prospects for the equipment suppliers. Demand from the cloud customers does brighten up the picture, but whether equipment suppliers can capitalize on this opportunity remains to be seen.

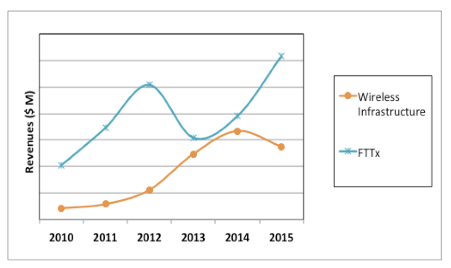

Market for optical components and modules has completed its sixth consecutive year of growth, with growth averaging 14% in 2010-2015. The growth rate in 2015 was 15% – a slowdown compared to 25% in 2014. Sales of FTTx transceivers and BOSAs were up by a staggering 58%, compensating for an 18% drop in sales of wireless fronthaul optics. The FTTx and wireless segments are greatly impacted by demand for these products in China and tend to fluctuate wildly, depending on the situation in that country, as shown in the Figure .

Excluding the FTTx and wireless segments, the global optical transceiver market was up 11% in 2015, averaging to 9% CAGR in 2010-2015. The analytics projects 18% growth in 2016 and 12% CAGR in 2016-2021, but this forecast hinges on the adoption rates of several new technologies:

- 100G Ethernet and DWDM optics

- Flex-grid WSS modules

- 16G Fibre Channel

- 25G line rate AOCs and EOMs

100 DWDM and 16G Fibre Channel products will be in their 3rd year of deployments in 2016, but all other products listed above are just entering the broader market and uncertainty is high.

100GbE QSFP+ transceivers are selling briskly in early 2016, but it is still unclear how many of these will be purchased by operators of mega data centers this year. Introduction of 50GbE and 200GbE to the industry roadmap adds uncertainty.

Sales of WSS modules, including new flex-grid products, picked up late in 2015, suggesting that the next round of upgrades is starting in metro and long-haul networks. How many service providers will join this round remains to be seen.

2015 was a good year for Active Optical Cables (AOCs) and Embedded Optical Modules (EOMs). Ericsson and Oracle had demonstrations of new systems based on EOMs at OFC 2016. Several operators of mega data centers are planning to use 25G AOCs in 2016. It is time for the AOC/EOM market to embark on steady growth after many ups and downs over the last decade.

The markets for FTTx and wireless optics will continue to depend on the situation in China, but adoption of next generation products will be important as well.

Demand for 10G PON started to pick up in the second half of 2015 and projections for this year are optimistic. However, we have seen sales of these products start up for a quarter and then drop to zero for the next 2-3 quarters in 2012-2014. We project for a steady growth in 2016-2021, but fluctuations in demand are still likely.

Several equipment vendors introduced DWDM fronthaul solutions in early 2016. One U.S. service provider plans to deploy it this year while many others are evaluating it. Sales of higher priced 10G DWDM optics should give a boost to the wireless fronthaul market in 2016-2021. The technology is ready, the products are available, it is up to the service providers to pull the trigger.