Four times a year, the reseach team collects company financials and operating metrics from across the optical communications value chain, and they receive proprietary shipment data from more than 20 optical components vendors. They review the data, compare it to our existing forecasts, and tell clients what is happening in the market, in the form of a Quarterly Market Update.

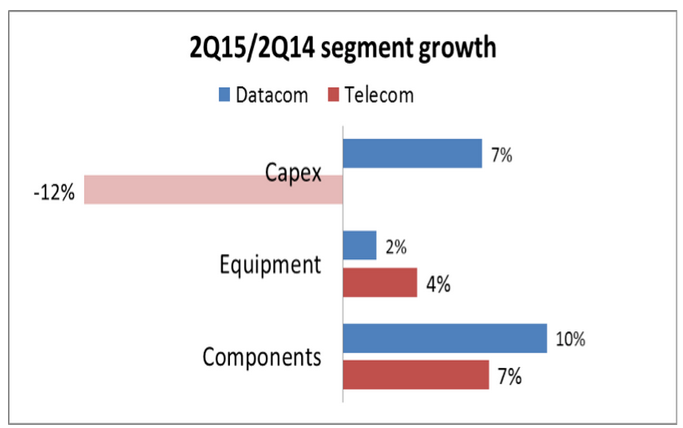

The just-published September 2015 update reflects their analysis of financials and vendor shipment data through the first half of 2015, and industry news through Q3 2015. This graphic from the report summarizes the growth in service provider capex, and equipment and component vendor revenues, for 2Q 2015 compared to 2Q 2014.

It’s clear that telecom service provider capex fell off in the first half of 2015 compared to 2014, due to completion or tapering down of some large deployment projects around the globe, including China Mobile’s LTE deployment, Vodafone’s Project Spring, and Sprint’s Network Vision. Mega-datacenter operators on the other hand increased spending by 7%, which although positive, is smaller than the double-digit growth rates we are used to seeing for this group.

Equipment maker revenues grew a scant 2% and 4% in the datacom and telecom segments, respectively. ‘White box’ makers continue to make inroads in the datacenter equipment segment, while on the telecom side, Huawei’s and ZTE’s market shares gallop upward, and those of other incumbents languish. Pricing pressure continues to weigh heavily on revenue growth. Keen interest in Software Defined Networking and Network Function Virtualization may also be a factor in dampening equipment demand, as service providers take a breather to rethink their network plans.

2Q15 sales growth among optical component companies was a little better than at the equipment level, with datacom up 10% and telecom up 7%. One of the main reasons for this is the growing adoption of 100Gbps components, which carry a higher price tag than slower speed devices.

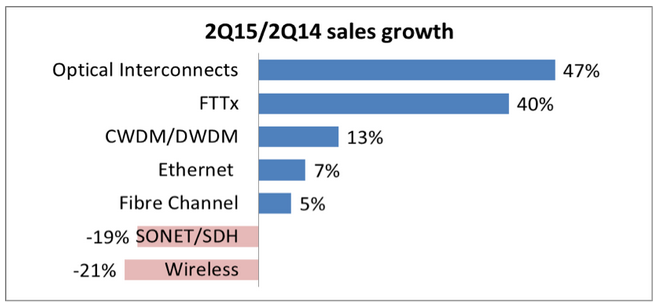

The second chart (below) shows 2Q 2015 sales growth for the main product categories that we forecast. Ethernet and WDM are the two largest segments in terms of revenues, and both grew at a respectable/healthy rate. Optical interconnects continued to show rapid growth but are still a very small segment, totaling a little over $50 million in sales in 2Q 2015. FTTx also experienced high growth, driven by an acceleration of China’s broadband plans. The wireless segment on the other hand was down considerably, but that was to be expected given the extraordinary amount of LTE gear deployed by China Mobile in 2014.

They projected total optical transceiver market growth of 25% in 2015. Subsequently, some public optical components companies gave rather soft guidance for the balance of the year in their 2Q 2015 earnings calls, and political developments in China have called capex spending there into question. Based on our analysis of the most recent data and news, they have also decided to soften their outlook for optical components sales in 2015, but only to the extent of reducing our forecast growth rate from 25% to 15%. Even at this lower growth rate, full-year 2015 industry revenues should set a new record high, above $4 billion. One of the reasons They did not reduce the outlook more is that we are seeing private companies growing faster than the industry average and winning market share from the larger public vendors.