It is hard not to get carried away with excitement about the optics market in 2016. Demand is at an all time high. Strong growth in sales of 100G DWDM and 100GbE products made a lot of headlines this year and expectations for 2017 are high. However, analysis of the broader market for optical components and modules uncovers a few problems. Apart from DWDM and Ethernet optics, all other market segments are likely to remain flat or decline in 2016. This includes SONET/SDH, Fibre Channel, FTTx, wireless fronthaul and optical interconnects (AOCs and EOMs).

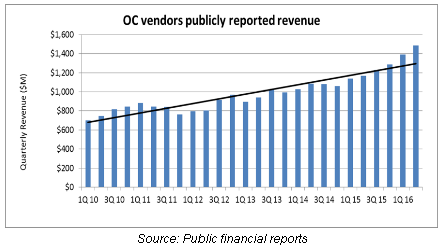

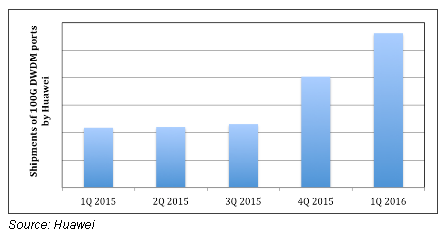

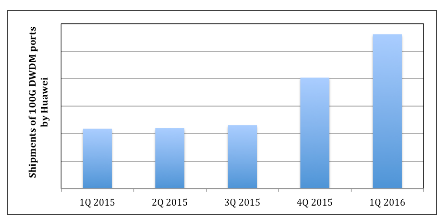

The total market for optical components and modules is expected to grow by 17% in 2016, with sales of DWDM and Ethernet products increasing by more than 30%. Massive deployments of 100G DWDM networks in China and 40GbE/100GbE optics in mega-datacenters by cloud-based companies are the main drivers of market growth this year and beyond, as illustrated in the figure below.

The total market for optical components and modules used in optical communications will grow at a CAGR of 10% in 2017-2021. Sales of optics to the cloud datacenter market will continue to grow rapidly in 2017-2021, averaging 20% annually.

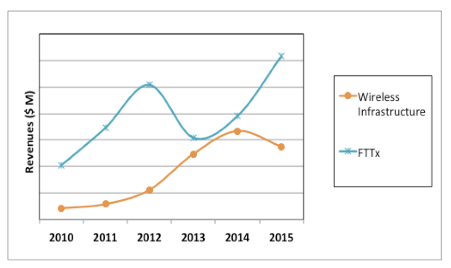

The increasing contribution of China to the global market was related to its massive deployments of FTTx and wireless fronthaul optics in 2011-2015, but the situation has changed in 2016. This year it is demand for 100G DWDM and 100GbE optics that increased China’s share of the global market, and we think this trend will continue in 2017-2021.

The Market Forecast report provides a detailed market demand forecast through 2021 for optical components and modules used in Ethernet, Fibre Channel, SONET/SDH, CWDM/DWDM, wireless infrastructure, FTTx, and high-performance computing (HPC) applications. Key inputs include an analysis of the business and infrastructure spending of the top 15 service providers and leading Internet companies, and sales data from 2010 to 2016 for more than 30 transceiver vendors, including more than 20 vendors that shared their confidential sales information.